A Jeddah platform built to deliver Atlas fast — and to operate it long after handover.

Organizational overview

Xtopia Developments is the real estate development arm of the Xtopia group — a Jeddah-headquartered platform operating across the Kingdom's principal growth corridors: Riyadh, Jeddah, Mecca and Medina.

Why Xtopia delivers Atlas fast

A lean senior decision-making team, pre-existing delivery infrastructure and a consortium ready to mobilise compress the critical path from appointment to ground activity — directly answering the fund manager's expectation of a fast-tracked roadmap.

Senior-level relationships within the Amanah (Jeddah municipality) and relevant ministries give Atlas privileged early engagement on zoning, permitting and regulatory alignment — a core competitive advantage the RFP weights heavily.

STRONG PARTNERS

Track record — three success stories

Representative deliveries by Xtopia consortium partners.

Infrastructure delivery partner — Al Ojaimi Contracting

To deliver the horizontal infrastructure, Xtopia has an initial agreement in place with Al Ojaimi Contracting — one of the Kingdom's most established contractors. Al Ojaimi joins the consortium as both the infrastructure-execution lead and an equity-aligned delivery partner.

Atlas is an infrastructure-led serviced-land subdivision — elevated by community anchors that lifts blended land value across the whole scheme.

Xtopia enables the land through horizontal infrastructure, utilities and regulatory-ready plots — maximising plot value through a clear frontage hierarchy.

On a defined portion of the land, Xtopia and Arada develop vertically into a mixed-use, community-led destination — the engine that lifts blended land value across the entire scheme.

This is how Atlas becomes worth more than the sum of its plots: distinctive masterplanning and placemaking, not raw serviced land alone.

A deliberate efficiency trade: within the superstructure portion, efficiency is set intentionally below the 60% baseline — to make room for the lifestyle, community and public-realm elements that create the premium.

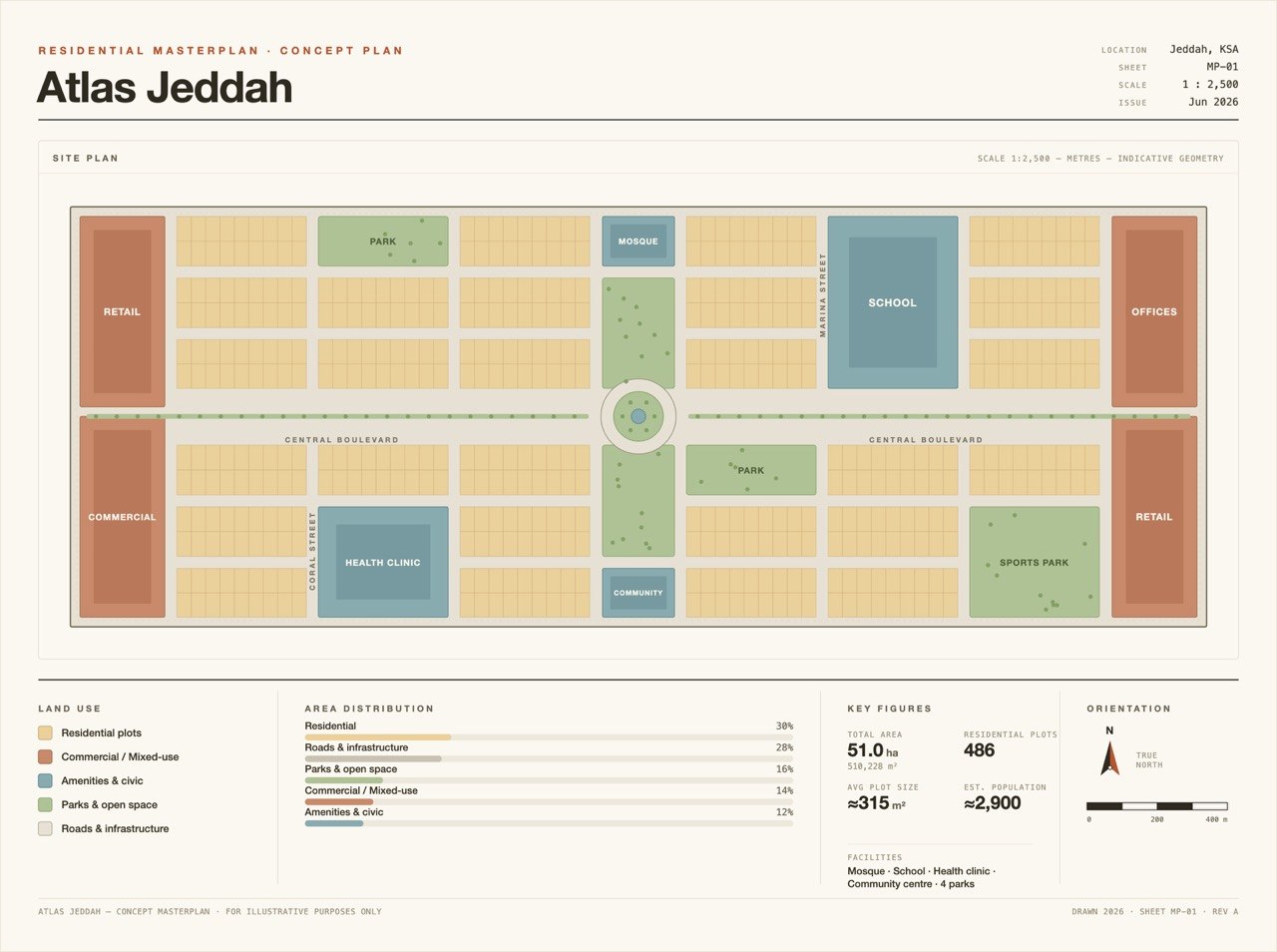

A confirmed site geometry, resolved into three measured land-use components.

Land-use structure (measured)

Indicative GFA applies a 70% building efficiency to each zone (land area × efficiency × floors). High-level assumptions pending the Colliers masterplan and validation.

A residential-led program with concentrated commercial frontage value.

Internal roads, utilities and public realm are accommodated within the residential parcel. Indicative GFA at 70% building efficiency. Confirm against the Colliers masterplan before issue.

An infrastructure-led base case — with a superstructure uplift in the aspire scenario.

Feasibility summary — Scenario A

Pricing & absorption rationale

most weightedPlot pricing is benchmarked against comparable serviced-land transactions along the King Abdulaziz / Al Safa corridors.

Benchmark rates shown as draft (dashed) — to be evidenced by Colliers comparables & absorption study.

Superstructure value uplift — Scenario B

The Arada superstructure overlay is the principal value-creation lever in the aspire case. The uplift comes from three compounding sources:

A fee structure aligned to performance — and honest about what is, and isn't, a project cost.

Fee structure

The distinction matters for the feasibility: only the 0.75% developer S&M fee sits in the cost stack; the 2.5% agent commission is borne by buyers and therefore does not dilute project returns.

Inclusions & exclusions

A fully-funded delivery structure — the consortium takes full equity, funds the build, and is repaid only as Atlas sells.

The Xtopia-led consortium takes full equity participation in the development — and critically, funds the development itself. Al Ojaimi Contracting carries the development cost on its own balance sheet and recovers monies owed from sales revenue as plots and built product sell.

A deliberately fast-tracked sequence — appointment to exit in approx. two years.

Senior Amanah and ministry relationships accelerate approvals, a consortium ready to mobilise shortens the gap between appointment and ground activity, and lean internal decision-making removes the delays that typically slow mandates of this scale.

A consortium where partner strength and superstructure value reinforce one another.